|

IP implications of EU customs law development We wanted to bring to your attention an important EU customs law development. That may sound like it doesn’t have much to do with IP, but it does! From 1 May 2016, EU customs legislation will begin to undergo a complete overhaul. One of the key changes relates to royalties and IP licence fees for goods imported into the EU. These changes will result in a significant increase in cases where those payments are dutiable and therefore need to be included in the customs value of the imported goods. This will in turn result in an increase in the amount of customs duty and import VAT payable on the goods. It is advisable to review how royalty/licence fees are structured for goods you import into the EU. If those payments will be caught by the changes we can provide advice on possible ways to mitigate that impact. In some cases that may involve making changes to the terms of your licence agreements. Further information is set out below. If you have any questions or would like to discuss how you may be able to best prepare for these changes, please do not hesitate to contact us.

Introduction On 1 May 2016, the European Union will begin the implementation of the Union Customs Code[1] (“UCC”) and its implementing legislation.[2] This legislation will replace the current EU customs legislation contained in the Customs Code and its implementing provisions.[3] One of the key changes[4] that will come into force on 1 May 2016 is that royalties and licence fees relating to goods imported into the EU will be treated as dutiable in more circumstances than under the existing legislation. From 1 May 2016:

What are royalties and licence fees? Royalties and licence fees are payments for the use of rights relating to (i) the manufacture of imported goods (e.g., patents, designs, models and manufacturing know-how); (ii) the sale for exportation of imported goods (e.g., trade marks, registered designs); or (iii) the use or resale of imported goods (e.g., copyright, manufacturing processes inseparably embodied in the imported goods).[5] Royalties and licence fees under the current legislation Under the current legislation, royalties and licence fees, which are not already included in the price of the goods and which the buyer must pay, either directly or indirectly, must be included in the customs value (i.e., they are dutiable) where the royalty and/or licence fee relates to the imported goods and where the buyer makes the payment as a condition of sale of the goods being valued. With regards to the ‘condition of sale’ requirement:

The current legislation also distinguishes between trademark royalties and other royalties and licence fees. In particular, trademark royalties require additional conditions to be met before such trademark royalties may be deemed dutiable. They will not be dutiable if the buyer of goods is free to source the goods from suppliers unrelated to the seller. Many companies have benefited from this exemption. Royalties and licence fees under the UCC Royalties and licence fees will continue to be treated as dutiable only where the rights are related to the imported goods and where the buyer makes the payment as a condition of sale of the goods being valued.[7] Royalties and licence fees are related to the imported goods where, in particular, the rights transferred under the licence or royalties agreement are embodied in the goods. The circumstances where a payment will be treated as a condition of sale are significantly broadened under the new legislation. Payments will be deemed a condition of sale where: a. the seller or a person related to the seller requires the buyer to make the payment; b. the payment by the buyer is made to satisfy an obligation of the seller, in accordance with contractual obligations; or

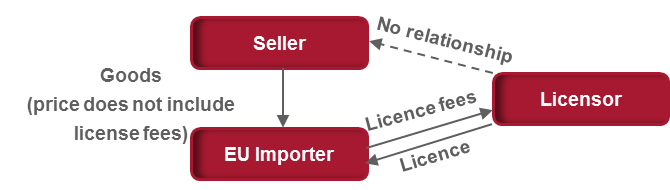

c. the goods cannot be sold to, or purchased by, the buyer without payment of the royalties or licence fees to a licensor.[8] [NEW CONDITION] As a consequence of the new condition contained in (c) above, royalties and licence fees that are paid by the buyer of the goods to a third party are much more likely to be a condition of sale (and therefore dutiable). The nature of the relationship between the third party and the seller will likely no longer be the deciding factor. Royalties and licence fees will now be dutiable even if the seller and the licensor are unrelated if the buyer cannot purchase the goods without these payments (e.g., if the goods would infringe the intellectual property rights of the third party licensor without such payments, this may be caught). The diagram below illustrates how the new condition (c) will affect businesses in practice. Diagram – Impact of new condition (c)

Post-UCC: The current exemption for trademark royalties will no longer exist under the UCC. This will result in trademark royalties being subject to the same rules as royalties and licence fees, as described above. What does this mean for companies importing into the EU?

The changes to the rules on dutiability of royalties and licence fees will result in a significant increase in cases where such payments need to be included in the customs value. This will in turn result in an increase in the amount of customs duty and import VAT payable on the goods.

Where the amounts of dutiable royalties / licence fees are not known at the time of import (e.g. the amount of the payments are dependant on the number of products sold), this will result in additional challenges for importers as the value of the goods at the time of import will be provisional. This will mean that the importer will need to agree with the customs authorities on how to treat such entries and whether / how the final customs value is to be adjusted to take account of the final royalties / licence fee payments. The challenge is that there is no consistent approach across the 28 Member States as to how to deal with entries where the value is provisional at the time of entry. An importer will therefore likely need to negotiate with each Member State to agree the methodology for reporting value adjustments. Whilst this is already a challenge for companies that have dutiable royalty / licence fee payments where the amounts are not known at the time of import, this challenge will arise for companies much more frequently under the UCC as the circumstances when such payments are dutiable will increase.

In preparation for the implementation of these changes on 1 May 2016, importers should review what royalties and licence fees are payable in respect of goods which they import into the EU and consider whether these payments will be caught within the scope of the new rules. If so, consideration should be given as to whether there are any ways to mitigate the impacts of this change. This could include, for example, considering (i) whether the royalties and licence fees “relate to” the imported goods; (ii) whether all the payments are dutiable or whether apportionment into dutiable and non-dutiable elements might be possible; and (iii) potential rewording of royalty and/or licence fee agreements. * * * The foregoing is intended only to provide an overview of changes to royalties and licence fees under the Union Customs Code. If you have any questions or if you require advice on any specific transactions or plans, please contact one of the members of Baker & McKenzie’s Customs Practice Group. * * *

[1] Contained in Regulation (EU) No 952/2013, together and its corresponding Delegated Act and Implementing Act. [7] Art. 71(1)(c) UCC. |